Growth

Q1 Review of Group Selection (GS) Scores

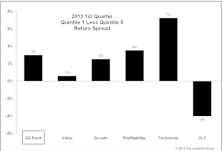

After a recent rough patch due to a multitude of factors (macro driven markets, high correlations, etc.), our domestic Group Selection (GS) Scores started seeing more consistent performance during the fall of 2012. This continued through the first quarter of this year, with the Attractive to Unattractive return spread at +3.0% year-to-date.

Factor In Focus: Asset Growth Identifies Lack Of Capital Discipline

Asset growth is a factor that gets some attention, but not nearly as much as other more mainstream factors like price to earnings, earnings growth, etc.

A Closer Look At Growth And Value Return Differences

Traditional Fama/French analysis shows an exceptionally large 4% per annum return edge favoring Value. Based on Russell 1000 Growth and Value Indexes, however, the edge in favor of Value has been a fraction of that. Current year’s Growth outperformance is also dissected to determine the likelihood this leadership will persist.

Where To Invest? A Graphical View of Global Equity Markets

Taking into account the variety of total return contributors, we conclude that no one regional equity market stands out as a slam dunk investment idea.

New Dividend Growth Screen

A new dividend growth screen and another that additionally incorporates dividend growth at a reasonable price are explored.

Global Perspective On 2012 Earnings, Sales, and Margins

Leuthold’s Eric Weigel dissects earnings, sales and margin expectations for the coming year.

The Return Of Value And Growth?

Correlations finally drop during the October market rally. Both Value and Growth factors outperformed during the month. Some momentum factors have diverged… each is an atypical occurrence.

Two Quant Themes With Significant Implications For 2011

Two Quant Themes With Significant Implications For 2011. We revisit studies from the past year that focused on Revenue Growth vs. Earnings Growth, as well as Momentum vs. Value.

Popularity, Agreement, And Trust: A Global Perspective Of Investor Preference

Analysts are playing an increasingly important role in today’s market. In this section, we focus on the market’s interpretation of three characteristics related to analysts estimates: Popularity, Agreement, and Trust.

Revenue Revival: The Key To Sustained Earnings Recovery

Jim Floyd examines the revenue growth of the ten broad sectors in this month’s “Of Special Interest”.

Bull Markets: The Best Comes First

New bull markets are front end loaded, with the strongest performance usually coming within the first few months. Study also shows that Small Cap Growth stocks tend to outperform their Large Cap and Value counterparts.

Can Growth Stocks Outperform Value In A Bear Market? You ‘BETA’ Believe It!

Conventional wisdom and modern day historical evidence indicate that Value stocks do better in bear markets. But from the 1920s through the 1970s, it was Growth that held up best during bear market declines.

Large-Cap Growth: Could A Long Wait Get Even Longer??

Valuations set the stage for better performance out of growth. But it is important to note that there’s precedent for the value cycle—seemingly already overextended in time and price—to get much more extended.

A Closer Look At 2007 Projected Earnings Growth

Initial results for Q1 earnings look disturbing. Analyst estimates of 2007 year end earnings for stocks have been declining across all market cap tiers, with biggest declines in the Energy sector.

Modifications To Leuthold Growth Versus Value Methodology

We have modified our Small Cap and Mid Cap Growth versus Value methodology, improving the algorithm for distinguishing between growth and value to make the components more reflective of these sectors.

High P/E Stocks: Becoming A Safe Place To Hide?

Value continues to have leadership position over Growth among Large Cap stocks. Mid Caps also shifting to favor Value, but Growth still leading in the Small Cap tier.

Cyclical Stock Dominance — How Long Can It Persist?

An in-depth examination of performance relative to Growth stocks; what has been typical in terms of leadership duration; and how the economy and inflation may affect the current trend.

What Is Driving S&P 500 Earnings Growth?

The Energy sector is really driving S&P 500 earnings Growth.

Looking For Earnings Disappointments.....Before They Hit The Fan

New Improved Potential Earnings Disappointments Screen: Inventory Growth Versus Sales Growth.

Analyzing Large Cap, Mid Cap & Small Cap 2004 Composite Income Statements

2004 earnings very strong but further earnings improvements in 2005 will be largely a function of stronger sales, not any more margin expansions.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue