Articles by Greg Swenson Director of Equities

Rankings At The Top Offer Diversified Mix

Energy remains the top-rated sector, but Information Technology, Communication Services, and Financials follow closely behind. These offer a diverse mix of commodity, growth, and cyclical options.

Leuthold Select Industries Portfolio

Select Industries has overweight positions in Energy, Materials, Consumer Discretionary, and Industrials. The portfolio has no exposure to Consumer Staples, Real Estate, or Utilities.

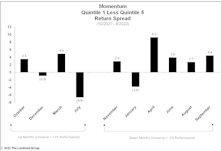

Losing Momentum

After working well in 2022, Momentum took a beating out of the gates in 2023. Investors rejected the winners from last year and returned to the lowest quality and most speculative winners from the previous low-rate playbook.

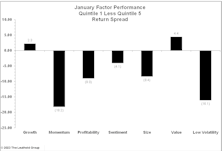

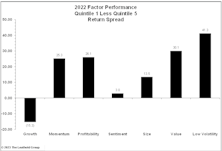

2022 Quantitative Factor Performance: Year In Review

The rotation into Value continued into 2022, with Momentum joining the party and Growth the only blemish on the factor scorecard.

Momentum Offering Downside Protection

In a volatile year, protection is coming from what many may deem an unlikely suspect—the momentum factor. Contrary to popular belief, momentum tends to work better in down months than up months.

Fully-Invested Portfolios - October 2022

AdvantHedge has performed better than the inverse S&P 500 and the inverse Russell 2000. Markets cascaded lower during the month as hotter than expected inflation reports pushed expectations higher as far as future Fed rate hikes.

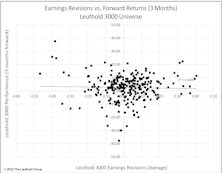

#53 - Earnings Revisions And Predictive Power

While the market moves back into sell-off mode, everyone seems to be waiting for the inevitable hammer to drop on earnings. If and when that happens, does it give us any insight about performance prospects? Or does it just make forward P/E ratios less attractive?

Earnings Revisions And Predictive Power

While the market moves back into sell-off mode, everyone seems to be waiting for the inevitable hammer to drop on earnings. If and when that happens, does it give us any insight about performance prospects? Or does it just make forward P/E ratios less attractive?

Fully-Invested Portfolios - September 2022

AdvantHedge was up 3.5% in August, trailing the inverse S&P 500 (+4.1%), but ahead of the inverse Russell 2000 (+2.1%). It was a tale of two halves for this equity hedge last month.

Tactical Asset Allocation Portfolios - September 2022

Both the Leuthold Core and Leuthold Global portfolios did a good job mitigating losses during the August selloff thanks to low equity exposure and relative outperformance from the stock holdings.

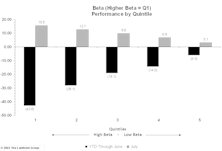

High-Beta Bounce

High-beta stocks outdid everything else during July, after getting crushed during the first half of 2022. At the end of June, Momentum was more correlated with low beta than any other time in our history.

Factors Reverse Alongside Market

With equities rallying off bear market lows, factors also reversed during July. Except for Profitability, every factor category performed inversely to their year-to-date results. Momentum and Low Volatility were the biggest losers, while Growth was the biggest winner.

Fully-Invested Portfolios - August 2022

AdvantHedge was down 10.1% in July, trailing the inverse S&P 500 (-9.2%), but ahead of the inverse Russell 2000 (-10.4%).

Tactical Asset Allocation Portfolios - August 2022

Both the Leuthold Core and Leuthold Global portfolios participated in July’s equity rally, but lagged their all-equity benchmarks.

Sector Rankings

See this month's sector rankings.

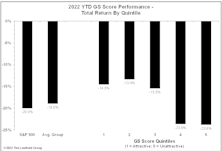

Energy Strength Is Intact; GS Scores Continue To Produce Positive Results

Energy has solidified its spot atop the GS Scores; it’s by far the highest-rated sector and counts three underlying groups among the top-ten industries out of all the sectors. Valuations have only improved amid steady outperformance, and renewed capital discipline looks to remain for the foreseeable future.

Fully-Invested Portfolios - July 2022

AdvantHedge was up 7.5% in June, trailing the inverse S&P 500 (+8.3%), and the inverse Russell 2000 (+8.2%).

Tactical Asset Allocation Portfolios - July 2022

Both the Leuthold Core and Leuthold Global portfolios saw negative performance in June, as the underlying equity portfolios underperformed their benchmarks. Fixed income and gold also sold off.

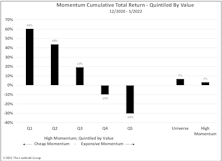

Reversal Of Fortune For ValMo Investors

From the end of 2020 through May, stocks in the top quintile of both value and momentum have returned 60% versus 7% for the overall universe. That compares to the brutal stretch from 2016-2020 when the only way momentum investing worked was to not only disregard valuations, but to actively buy the most expensive momentum stocks.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue