Macro Monitor

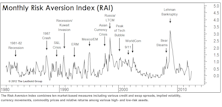

RAI Rose Again And Stays On “Higher Risk” Signal—Remain Cautious

The RAI rose in May and stays on a “High Risk” signal. We remain cautious and recommend higher quality within fixed income.

Inflation Slides Again

April inflation numbers were generally lower than expected. We are shifting out our inflation outlook by six months. We believe inflation will be a non-factor for the next six months but will increase moderately in the following six months.

10-Year Still Range Bound Between 185-245 But Expect Higher Volatility

We think the 10-year yield will likely consolidate around 200-215 before taking a shot at 245. The 245 level looks like a strong barrier and will likely hold in the foreseeable future.

Global Yield Curve Confirms “Muddle Through” View

The global yield curve is in a sideways range bound pattern, indicating anemic demand for credit. An examination of developed and emerging countries confirms our “muddle through” view.

Weaker Currency = Higher Net Exports? It’s A Myth

In the medium term (1-2 years), weaker currency actually leads to lower net exports because export prices go up, instead of down, when currency depreciates.

"Muddle Through"

The global economy is stuck in a “muddle through” mode with developed and emerging countries showing divergence in terms of leading indicators. Despite this divergence, they share one thing in common: an upturn in inflation. How much more room there is for easing is a key determinant of asset market performance.

Implications Of The End Of Negative Real Yield

The 10-year real yield turned positive at the end of 2012 and has stayed there. We expect higher interest rates, a stronger dollar, and lower gold prices in the next twelve months.

The Weakening Yen — Too Far Too Fast

We are highly skeptical “Abenomics” can produce different results this time.

The Upside Breakout

We still think interest rates are likely to be range-bound, but the range will likely shift higher to the 185-240 bps area if the current breakout is successful.

New “Higher Risk” Signal — But We Remain Cautiously Optimistic

We’re downplaying the new signal’s significance and remain cautiously optimistic towards risky assets near term. Our biggest concern is that a rise is extremely likely going forward.

The State Of Interest Rates

We think interest rates will stay low for an extended period of time, so the key question is, when will rates start rising?

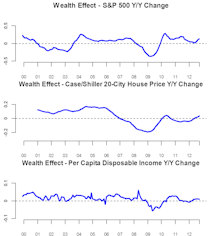

Wealth Effects: Housing Likely To Be The Bright Spot

The stock market wealth effect has been direct and pronounced. But it’s been wearing off, with the subsequent rally after each Fed stimulus weaker than the previous one.

QE3 Is Ill-timed And Should’ve Been Saved For A Greater Risk Event

What is the Fed going to do if another risk event hits and the S&P goes down 15-20%? Pray?

Not So Calm In The Bond Market

The failed break-out to the upside on the U.S. 10-year yield fits our expectation of a range-bound but higher-volatility environment.

Lowered Expectations — Policy Effectiveness

For central bank policy effectiveness, global economic growth, interest rates, and inflation. While lowered expectations are a good thing in the near term, long term return expectations for most asset classes should be lowered too.

Risk Aversion Sharply Lower—But Optimistically Cautious

We remain optimistically cautious, as we believe the determination of the policy makers to prop up the market should not be underestimated, especially in an election year.

Bi-Modal Or Middle Of The Road—We Think The Latter

How do we avoid volatility in a high Uncertainty/low conviction world? We compare a “bi-modal” portfolio of 50% Treasuries/50% High Yields with a “middle-of-the-road” portfolio of 100% Investment Grade Corporate bonds. The latter wins in both good and bad scenarios.

2012 Time Cycle—Mid Year Update

1st half LT rate movements tracked cycle composite well, but we differ on the pattern in the second half. The “muddle through” pattern on the U.S. Composite Leading Indicator is more consistent with our view.

How Low Can It Go? Watch The Bund Yields

Going forward, at least in the near term, we think a good guide for the potential downside on U.S. interest rates might be the German bund yields.

New Higher Risk Signal Generated But Optimistically Cautious

This new “Higher Risk” signal closed out the previous “Lower Risk” signal generated last December, and this measure is telling us it’s time to play a little defense.

Perception for the Professional

May 2026 Issue

Featured Articles

Sector Navigator

May 2026 Issue