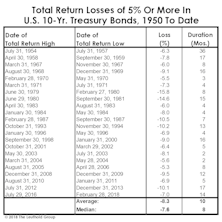

Treasury Bonds

Bond Yields: Cyclical Pressures Vs. Positioning

.jpg?fit=fillmax&w=222&bg=FFFFFF)

Even after watershed events COVID-19 and MMT, some things never change.

Next year will begin like almost every one of the past dozen years, with economists and strategists expecting bond yields to rise.

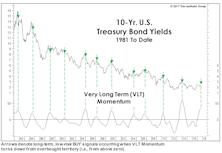

Unlike most of those years, though, there are several measures of “cyclical pressures” that would seem to give them a good chance of being right. The best-known among these might be the “Copper/Gold Ratio,” popularized by DoubleLine’s Jeffrey Gundlach, which suggests 10-Yr. Treasury yields should be around double their current level (Chart 1).

“Unlevered” Treasuries Aren’t A Bubble

It’s been popular to argue that U.S. government bonds are a bubble while U.S. equities are not. But even if we agreed, the potential cyclical total return losses in Treasury bonds are a fraction of those likely to occur in an equity bear market.

The Bear Market No One Discusses

.jpg?fit=fillmax&w=222&bg=FFFFFF)

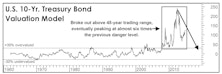

Yields on 10-year Treasury bonds have still not breached the 3.00% level that many believe will stick the proverbial “fork” in the secular bond bull market that began in 1981. That could well in happen in the next few weeks, but we believe it’s important to step away from the daily fray and reflect upon the damage that’s already been done.

Four Divergences—A Steepening Correction

While we still believe flattening is the more likely scenario over the medium term, we do feel the recent flattening move is a bit overdone and there are several divergences that suggest a short-term steepening correction is in store.

A Mysterious Bond BUY Signal…

Sometimes we feel compelled to report findings that conflict with our outlook. And then there are the even rarer times we actually do it.

Hare Passes Tortoise

Last week we overlooked a key milestone among the daily parade of new stock market highs: The Stock/Bond Total Return Ratio finally exceeded its cyclical high from the summer of 2007. Since July 13, 2007, the S&P 500 has generated a cumulative total return of +73.5%, just ahead of the U.S. 10-Year Treasury Bond total return of +70.0%. These work out to annualized returns of around 6.0%.

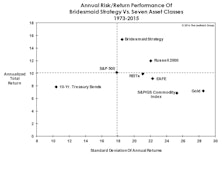

Bridesmaid Asset Strategy

Liquidity “consuming” strategies like price momentum are generally considered to be more volatile than liquidity “providing” approaches like value investing.

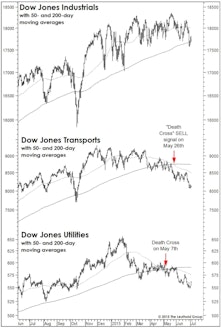

A BUY Signal That Says SELL?

Last month we discussed the negative market implications of May’s “Death Cross” signals in the Dow Transports and Dow Utilities.

What To Do With Broken Models?

With the quantitative horsepower now available at the fingertips of even the most technophobic portfolio manager, there’s little tolerance for any model that finds itself out of sync. But “broken” models (and especially value-based ones) have an eerie way of reasserting their relevance just after they’ve been finally tossed to the trash heap.

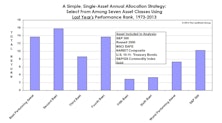

Buy The Bridesmaid, Not The One Looking To Rebound

The investment leadership of a given year has historically had better-than-even odds of outperforming in the following year at both the asset class and equity sector levels.

The Math Doesn’t Work For Long-Term Treasuries

The recent upside breakout in the U.S. 10-year yield was successful, and it appears interest rates will remain in the new higher range for now. But what are the short-term implications of higher U.S. Treasury rates on asset allocation decisions?

The Upside Breakout

We still think interest rates are likely to be range-bound, but the range will likely shift higher to the 185-240 bps area if the current breakout is successful.

The State Of Interest Rates

We think interest rates will stay low for an extended period of time, so the key question is, when will rates start rising?

Chasing Income That Barely Exists

Those adopting LDI today are doing so at the least opportune time in more than 60 years.

Not So Calm In The Bond Market

The failed break-out to the upside on the U.S. 10-year yield fits our expectation of a range-bound but higher-volatility environment.

The Reach For Yield… And Its Consequences

Investor infatuation with portfolio income is higher than ever, just as there is less of it available than at any time in history.

The Bubble In Bonds...

Yes, we consider U.S. Treasury securities a bubble across the entire yield spectrum, and the situation has probably now moved into “extra innings” (think 10th or 11th) thanks to the flight to (perceived) quality triggered by the European debt crisis.

Start Of A New Bond Bear Market Or Not, There Is No Need To Rush

Whether it’s the start of a new bond bear market or not, there’s no need to rush... and why shorting bonds may not be the best idea, even during a bond bear market.

Bonds: Beginning Of The End?

Today’s bond market is reminiscent of the stock market in April 2000—when the first cracks in tech and telecom had appeared.

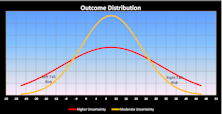

Looking Deeper Into The Tails Of Distribution

Leuthold’s Eric Weigel examines both positive and negative tail risk among asset classes over two time periods… the recent volatile era versus a preceding, not-as-volatile time period.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue