Profit Margins

A Spectacularly Average Thirty Years

In the spirit of good holiday cheer, we made a partial concession to the True Believers with a December “Chart of the Week” in which we narrowed our stock market valuation analysis to the historically elevated levels of last 30 years.

Allocation Implications Of Full Employment

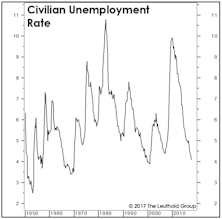

While the economy’s move above its full-employment level carries reliably negative implications for profit margins, the impact on equity returns has varied greatly from cycle to cycle.

An Economy This Healthy Is Hostile To Profits

.jpg?fit=fillmax&w=222&bg=FFFFFF)

It’s hard to grow profits when an economy’s resources are already fully employed, a fact we highlighted when the U.S. Output Gap turned positive several quarters ago. Therefore, the first quarter drop in NIPA corporate profits, reported yesterday, shouldn’t have come as a surprise.

Margins Prove Capitalism Still Works

.jpg?fit=fillmax&w=222&bg=FFFFFF)

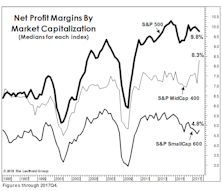

Corporate profits were outstanding last year, but even the benefit of a 40% cut in the top income-tax rate wasn’t enough to lift the net profit margin back to the all-time high of 10.6% established in early 2012. Still, the latest 10.0% figure is more than a percentage point above the 2007 cycle high and about two points better than any other cycle high.

They Can’t Tax What’s Not Earned

With three quarters of a sharply lower corporate tax rate on the books, the median four-quarter trailing profit margin for both the S&P 500 and S&P MidCap 400 jumped to all-time records in the third quarter.

What Can Margins Do For An Encore?

.jpg?fit=fillmax&w=222&bg=FFFFFF)

A massive drop in corporate tax payments lifted the third quarter NIPA profit margin back to the 10% level for the first time four years. But while we try not to always view the glass as half empty, we find it troubling that margins remain well-below their 2012 highs (10.6%) in spite of this one-time windfall.

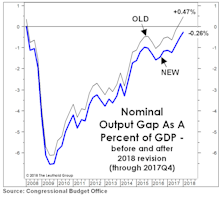

The Gap Is Back!

We celebrated the official closure of the GDP Output Gap in December, but that milestone was revised away in April by the statisticians at the CBO through a downward adjustment to the estimated rate of “full employment.”

Musings On Margins

Fourth quarter earnings were the last ones to be burdened by a 35% top marginal corporate income tax rate, and therefore seem to have been given a pass by the analyst community.

Multiple Contraction—Just A Little Patience?

Things were bigger when you were a kid. Like that enormous sweatshirt your aunt gave you for your birthday or that hand-me-down ten-speed bike with the cross bar taller than your shoulders.

The “Gap” Is Gone. Now What?

In Q3, the CBO’s Nominal Output Gap swung to positive for the first time since the last business cycle peak. This type of move has historically meant the cyclical peak in profit margins is close at hand.

Sector Margin Checkup

U.S. companies hoping for a reduction in the corporate tax rate are not exactly doing a convincing job of demonstrating “need.”

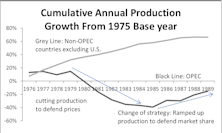

Recent Years’ Oil Price Experience Akin To 1980s’

We revisit commentary we published in 2015 regarding the late-2014 oil price crash and review why, at that time, we believed oil prices could stay at depressed levels for a longer period than most expected. Additionally, we advise avoiding two Energy sector segments: companies with high balance-sheet risk, and Energy Royalty Trusts.

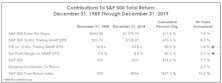

How To (Almost) Double Your Money In Under Ten Years

Buying the S&P 500 on one of the worst possible days in history ultimately yielded a total return of +87.4% (+6.8% annualized) through the end of April 2017...darn, sounds like an advert for Vanguard!

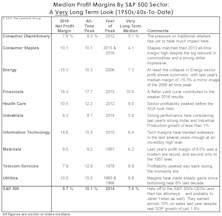

Sector Profit Margins: A Long-Term Review

Despite real GDP growth of just 1.6% in 2016, the median S&P 500 company earned a net profit margin of 9.7%, only 40 basis points below the record high established in 2014.

“Trailing” EPS Revisited

The S&P 500 trailing P/E has just climbed above 25x—lower than in March 2009—but incredibly high for any period in which earnings weren’t tainted by recession.

Valuations: The Correction That Never Was

The correction failed to meaningfully “reset” any long-term valuation measures, hence, we don’t view the current environment as having much investment merit, but rather, primarily speculative appeal.

Profit Margins At The Sector Level

S&P 500 profit margins mask the disparate trends taking place on a sectoral level. We dissect those trends with the ten major sectors grouped by five broad themes: Cyclicals, Commodities, Defensives, Interest Sensitives, and Tech/Telecom.

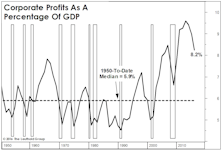

Margins: Mean-Reversion Works

A late March issue of The Economist proclaimed “profits are too high” and “America needs a giant dose of competition.” Funny. NIPA Corporate Profits figures released that week show The Economist’s plea for lower profits had already been fulfilled—and not just in the latest quarter.

Implications Of Low Growth, Low Inflation, Low Rates

The current environment will likely persist longer than most expect which will put further downward pressure on profit margins. As margins come under pressure, companies increase leverage to prop up ROE. However, the market wants higher duration, not higher leverage.

To Play The Rally, Or Not To Play?

Question: What will you do if the Major Trend Index returns to its bullish zone?

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue