NYSE

NASDAQ & NYSE Short Interest

Both the NYSE and NASDAQ short interest ratios saw increases in July.

NASDAQ & NYSE Short Interest

While the NASDAQ short interest ratio continued to decline, the NYSE ratio increased in June.

NASDAQ & NYSE Short Interest

Both indicators drop to neutral in May.

NASDAQ & NYSE Short Interest

Both the NASDAQ and NYSE short interest ratios increased in April.

NASDAQ & NYSE Short Interest

Both ratios still bullish.

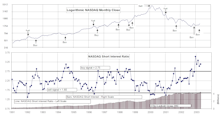

NASDAQ & NYSE Short Interest

Both ratios reconfirming a buy signal.

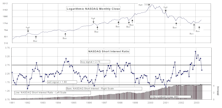

NASDAQ & NYSE Short Interest

NASDAQ ratio declines on increased volume. A new style this month gives the NYSE ratio more timely signals.

NYSE Moving To Westchester Is Not Nearly Enough

This month’s feature was written by Don Weeden, still a Maverick and Innovator! Named one of the fifty most significant people in the securities business since 1950. “…...The world’s premier market center remains dangerously exposed. A move to Westchester won’t diminish the danger.”

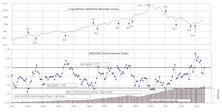

NASDAQ & NYSE Short Interest

NASDAQ record high short selling. NYSE moving to new highs.

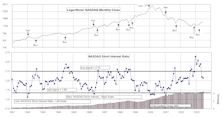

NASDAQ & NYSE Short Interest

NASDAQ ratio was flat for May while the NYSE's showed a very strong positive.

For The Technicians

Examining some of the impacts that decimalization and the inclusion of financial derivatives may have on the NYSE Advance/Decline Line & ARMs Index.

View From The North Country

“What? You’re buying MORE Junk Bonds?!” “Regulation FD” could ultimately improve the depth and quality of analyst research, turning the focus back to more relevant, longer term outlooks. “Sell Side” Stock Research: The reasons why we no longer use it.

The Growth In NYSE Stock Listings

Since 1990, the number of listed stocks on the NYSE has increased by almost 90%. This surge in the number of listings can have a significant impact on a great many tools of the technician’s trade.

Brought To You By Your Friends (?) At the New York Stock Exchange

In recent months, two studies have been released on the subject of program trading, particularly index arbitrage. One concludes that index arbitrage activities do no real damage. The other tells it like it really is.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue