Intrinsic Value

Speculating In “The Nebs”

One measure of a bubbly bull market is the degree of speculative fervor embedded in the prices of companies with nebulous, indeterminate, or even nonexistent intrinsic values. Since the bear market low in March 2020, speculative manias have evolved in a menagerie of asset classes including Innovators & Disruptors, SPACs, meme stocks, crypto currencies, and NFTs. Based on the breadth of valuation extremes across numerous and diverse assets, this bull market may rank second to none.

Valuation Extremes: Here Be Dragons

Top decile valuations are often the result of unduly positive investor sentiment that leads to inflated multiples. Bullishness comes in varying strengths: optimism, enthusiasm, exuberance, and, at the extreme, the mania of crowds. Because bullishness manifests itself in aggressive valuations for speculative companies, we believe the prices being applied to such companies - for which intrinsic value is dependent on a future that looks significantly different than today - are an excellent measure of investor sentiment. In that spirit, we examined past cycles of extreme valuations with the goal of understanding how they relate to investor sentiment and what they might tell us about market conditions and relative returns.

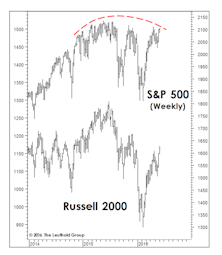

Rally Extension?

We’ve boosted equity exposure twice in the past several weeks, fully cognizant that it’s not a “textbook” time to do so.

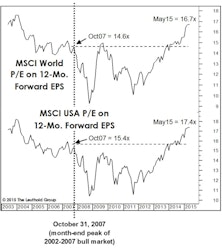

Valuations: The Correction That Never Was

The correction failed to meaningfully “reset” any long-term valuation measures, hence, we don’t view the current environment as having much investment merit, but rather, primarily speculative appeal.

The Bullish Case: A Mental Exercise

We’ve been correctly positioned near our tactical portfolios’ equity minimums, yet we’re oddly compelled to use this month’s “Of Special Interest” section as a very public second-guessing of that move.

Stock Market Valuation Check

It now goes almost without saying that whenever the stock market moves to a new cycle extreme, so does the MTI’s Intrinsic Value category. In late May, this reading dropped below –400 for the first time in this bull market, and is now within 150 points of its 2007 extreme.

I’m Still Afraid of Heights

Intrinsic Value benchmarks for each stock market average, using 1957 to date data. Using 1926 to date data the calculations are even more frightening.

The Mixed Messages Of January

It was a shaky 1998 start, but the U.S. equity markets got it together after the big hit on January 9th (-3%).

How High Is High?/How Low Is Low?

An update of The Leuthold Group’s Intrinsic Value Benchmarks provides a way of estimating upside and downside potential for the DJIA and S&P 500. How much higher might the stock market go in the next year…..and what is the bear market downside risk?

August Insights

Secondary stocks’ August performance, growth vs. cyclical and growth vs. value performance, S&P and DIJA historical valuations and the Royal Blue Index.

Inside the S&P 500, 400 and the DJIA

From time to time, there are client inquiries concerning the foundations of The Leuthold Group’s fundamental intrinsic value judgements, relating to the S&P 500, 400 and the Dow Jones Industrials. Here is a current data summary regarding these three stock market indices.

How High Is High?

The Leuthold Group’s Intrinsic Value Benchmarks provides another way of estimating upside potential for the DJIA and S&P 500. Based on the past history of bull market valuation levels, where might the stock market be 12 months from now?

Stocks Not Cheap, Stocks Not Expensive

Stocks are now in the high 40%-45% of the historical valuation distribution range. This is not cheap, but neither is it expensive. Based on our Benchmarks work, it now appears we can expect average performance for the stock market from today’s levels over 1, 3 and 10 year time horizons.

Continuing Client Questions

If the Index does shift to the positive side, how can you (in view of your own intrinsic value work) justify aggressively buying stocks? Considering the downside risk, is it really worth it to aggressively buy equities if your Index now turns positive? If your Index does turn positive, what are the chances it might be a whipsaw?

Client Questions About Our Equity Strategy

Most, but not all of these are actual client questions recently fielded by The Leuthold Group. A few are questions we think some of you might like to ask, but are reluctant to do so.

Projecting Stock Market Levels Using Intrinsic Value Benchmarks

How far would today’s stock market have to fall to achieve normal benchmark valuation levels? How far would it have to fall to reach 1987 post-crash levels? On the brighter side, how far up would today’s market have to move to match the valuation extremes of 1987’s third quarter?

Intrinsic Value Update

We apologize for the unanticipated Benchmarks delay. In the meantime, per client requests, here are updated histograms for our primary stock market value benchmarks, including commentary. We are pleased that so many of our clients really do use this work.

Well…November Was Better Than October

The cyclical bear market appears to be bottoming, but that is only an opinion. Although improved, the Major Trend Index remains negative. Thus, we remain very cautious. We respect the numbers more than our opinion.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue