Asset Allocation

Core & Global Portfolios Equity Exposure Increased Slightly In February

The Major Trend Index remains positive, and net exposure is 65% in the Core and 64% in Global.

Core & Global Portfolios Equity Exposure Maintained In January

The Major Trend Index remains positive and net exposure is 63% in the Core and 62% in Global.

Core & Global Portfolios Equity Exposure Maintained In December

The Major Trend Index remains positive and net exposure in both portfolios is 64%. For all of 2013, our average net equity exposure was 60% in each portfolio.

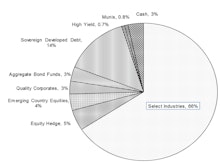

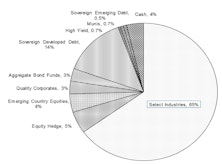

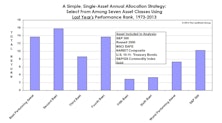

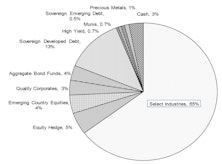

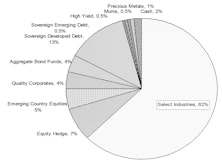

Buy The Bridesmaid, Not The One Looking To Rebound

The investment leadership of a given year has historically had better-than-even odds of outperforming in the following year at both the asset class and equity sector levels.

Core & Global Portfolios Equity Exposure Raised Slightly As Hedge Reduced

The Major Trend Index remains positive and, as expected, our temporary ETF hedge was lifted. Our net exposure in both portfolios is now 64%-65%.

Core & Global Portfolios Equity Exposure Trimmed Slightly To 60%

The Major Trend Index remains positive, but we reduced our target exposure from 62% to 60% using a short ETF as we believe this position will be temporary in nature.

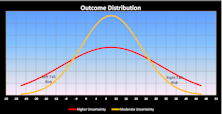

Looking Deeper Into The Tails Of Distribution

Leuthold’s Eric Weigel examines both positive and negative tail risk among asset classes over two time periods… the recent volatile era versus a preceding, not-as-volatile time period.

Buy Prior Year’s Winner, Loser, or Runner-Up?

The best strategy has been to buy not the prior year’s top performing sector or asset class, but to buy the runners-up—or “Bridesmaids”— of the prior year.

Asset Allocation: Still Heavy In Equities

Initial outlook for 2010 is to see the S&P 500 rise to 1300 or 1350 during the first half of the year but then give up those gains in the second half of the year. We are counting on the Major Trend Index to help navigate the choppy market.

Not As Bad As January...

First, let us be thankful February 29th only occurs every four years. No, we haven’t done a historical performance analysis of past leap year extra days, but you can be certain somebody now has. Whatever, it was a bad end to February 2008.

Initiated A Position In Japanese Equities

Used market weakness in Tokyo to begin building position in Japanese equities.

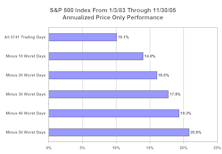

Debunking One Myth Of The Buy And Hold Rationale

Debunking one myth of buy and hold rationale. Showing how stock market returns change if investors avoid the best and worst performing stock market days. Essentially, anything can be proven with statistics.

A Look In The Rearview Mirror

What we did well and not so well...

View From the North Country

Stock market still considered lead economic indicator? Maybe not, considering the last three years, the stock market has been driven by Main Street. Changing role of portfolio managers: risk management function reduced to minimum if it even exists at all.

View from the North Country

Market timing: key to long term timing success is discipline. Politics 1996: the election outcome that minimizes prospects of decisive political action may provide the best market environment.

In Focus: Paid To Play

.PNG?fit=fillmax&w=222&bg=FFFFFF)

The Leuthold Group’s new direction in stock sector selection. A disciplined, unemotional, quantitative approach to today’s “real world” stock market group selection.

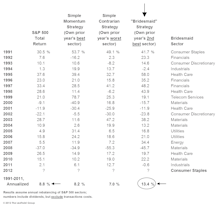

A Look In The Rearview Mirror

Self examination can be good for the soul, so each January time is taken to look back over the preceding year, critically reviewing the significant studies, portfolio shifts and recommendations appearing appearing in our publication.

Inside The Stock Market

On December 21, the Major Trend Index moved into "neutral" territory.

A Look In The Rearview Mirror

Self examination can be good for the soul, so each year time is taken to look back over the preceding year or so, critically reviewing the significant studies, portfolio shifts and recommendations appearing in this publication. Including the good...and the bad.

The Year That Was

1991 began on a grim note.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue