Articles by Scott Opsal Chief Investment Officer

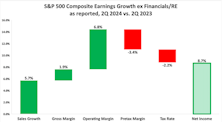

S&P 500 Earnings Waterfall 2Q24

Continuing strong GDP growth enabled S&P 500 member companies to post solid year-over-year results in the second quarter of 2024.

Research Preview: The Essence Of Quality

With renewed worries about the stock market, investors are pursuing safe-haven ideas—and Quality is a long-time favorite. Yet, despite its defensive appeal, the Quality factor has been a prominent bull-market leader, of late. Are the striking returns of Quality due to outsize exposure to the Mag 7—or have other high-quality stocks been equally fruitful in the latest upswing?

“Place Your Bets, Place Your Bets”

With Fed rate cuts likely to begin just days from now, the mathematical connection between changing rates and duration means that lower rates are almost certain to result in higher bond prices, an effect that has proven reliable since 2024’s high point in rates last April. The simple approach of targeting longer durations is complicated by today’s inverted curve, meaning that lower rates will almost surely not manifest themselves through a parallel downward shift in the curve, but will be accompanied by an un-inversion that will return rates to an upward sloping shape. This twist in the curve’s slope will require investors to target the appropriate spot on the curve to optimize the interest rate effect on bond prices.

Extreme Outcomes Beginning To Moderate

Domestic equities lost a little over 3% in the second quarter. Seven styles posted declines in that range, only to be countered by the continued outperformance of mega-cap growth stocks, which gained almost 10% for the quarter. This odd mix of returns left the S&P 500 up 4.3%, although that was clearly not the central tendency of equities in 2Q24

Research Preview: Do Fed Cuts Mean Easy Profits?

With multiple rate cuts nearly assured through year-end, investors can profit from the iron-clad link between changing rates and bond fund prices. But there are two circumstances that introduce complexity: 1) the yield curve will likely un-invert during this process, and the longest duration funds may therefore not experience the strongest price response; 2) potential changes in credit spreads may either enhance or diminish the duration effect felt by corporate bonds.

Styles, Boxes, and Paradoxes

Multi-cap funds face two paradoxes that introduce subtle hurdles into their fund analytics. While it is desirable for a fund to rely on a sound investment process and to follow that process consistently, a successful multi-cap fund might not be able to meet both desires simultaneously. Second, a successful multi-cap fund will always be compared to the highest performing peer group while unsuccessful funds will be compared to a less successful set of peer funds. Attentive fund analysts can overcome the challenges we have identified in this study, assuming they are cognizant of the unique issues facing multi-cap and mid-cap funds. This report is intended to arm analysts with just such insights to ensure that benchmark and peer group comparisons are meaningful and constructive.

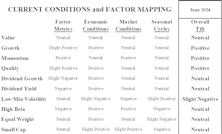

Factor Tilt Update

This month’s “Refresh” is the quarterly update on our factor regime analysis. Factors, or investment styles, have historically performed quite differently under various economic and market conditions, and we have mapped these relationships to identify which factors are best positioned for today’s environment. Second quarter factor returns continued the hot-and-cold pattern that has defined equity markets for some time now.

Research Preview: Defining The Mid-Cap Style

The unbounded nature of large-cap and small-cap styles means that they cover a great deal of territory, while mid-cap stands alone as a bounded style, and such limits significantly influence how a fund is classified. On the other hand, multi-cap is intentionally defined with wide latitude, but shares a style category with mid-caps, despite having little else in common.

Diagnosing Small Caps

After a strong period of market leadership following the internet bubble low of 2002, small cap stocks have been a great disappointment since 2016. Despite favorable economic conditions and a generally bullish market tone since the pandemic, small caps have failed to deliver on the hope of outperformance in a risk-on environment. As tactical investors interested in owning smaller asset classes when conditions are favorable, we are taking a fresh look at small caps, attempting to diagnose what has been ailing this market segment and what might be coming next.

Research Preview: Small Caps, Small Returns

Despite the overwhelming superiority of small cap returns, historically, during the winter months, the last three years have not followed the script. Three consecutive failures of this powerful seasonal influence make us curious if there are other market conditions that may be negatively influencing the smalls.

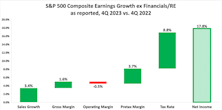

S&P 500 Earnings Waterfall 1Q24

Today’s eight largest firms produced an average gross margin of 65% over the last fiscal year, a 15-point gain since 1999—and pretax margins are truly amazing. The striking level of profitability at the top of the S&P 500 explains the top-heavy nature of the bull market, and at least partially justifies valuations.

Unlocking Value With “Name & Shame”

The financial performance of Korean companies has retreated to distressingly low levels in recent years. Consider that 67% of KOSPI index members trade at a P/B below 1x, and the median ROE is just 4.9%. To address the concerns of fading corporate performance, low valuations, and weak stock market returns, the Financial Services Commission joined with the Korean Stock Exchange to announce the “Corporate Value-Up” program in February 2024. The objective is to enhance corporate governance and shareholder accountability and to encourage companies to improve financial performance in the areas of P/B, ROE, ROA and shareholder payouts.

Surprising Strength For Active

Despite a hostile setting for active management in Q1, six of nine style boxes in our ongoing analysis achieved active-fund win rates above 50% (60% on average bested their passive benchmark). The other three each scored just below 50% of active strategies beating passive. This is remarkable given the proven importance of market conditions in the active/passive performance derby.

Research Preview: Korea’s Call To Action

Two of the most intriguing storylines across global markets in recent years concern Asian economies. The Japanese stock market provided the upside surprise, gaining a remarkable 64% in local currency terms since the end of 2020, making it one of the world’s top performers. On the flipside, South Korea ended April with a cumulative loss over the last three-plus years.

Comfort Food

Our March report titled Lifeboat Drill examined the effectiveness of sectors, styles, and factors in protecting investors during major market declines. We found that Consumer Staples are significant and consistent outperformers during times of distress, serving as “comfort food” for investors trying to minimize their financial and emotional distress in a falling market. Staples are relatively inexpensive today based on market-relative metrics, and today’s level of cheapness has historically corresponded to positive relative returns going forward.

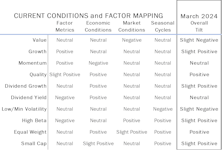

Factor Tilt Update

This month’s Leuthold Refresh is a quarterly update on our factor regime analysis. Factors, or investment styles, have historically performed quite differently under various economic and market conditions, and we’ve mapped these relationships to identify the factors best positioned for the environment at this time.

Research Preview: Staples’ Valuation

Well-respected analysts have been espousing different views on the Staples sector’s overall valuation. Some argue Staples is rather richly priced, while others believe it is a bargain in the making. Disagreement creates opportunities, and we believe a closer look at Staples is in order.

Lifeboat Drill

ETFs that focus on a single sector, style, or theme enable investors to make tactical calls that reflect their outlook and risk tolerance, resetting their risk/return profile to benefit from prevailing economic and market conditions. As fate would have it, the explosion of tactical, thematic funds that began 15 years ago coincided with a drought in market cycles. Following the Global Financial Crisis, the S&P 500 only experienced one moderate drawdown in the next nine years, meaning that opportunities to judge these new thematic ETFs during market declines were in short supply. This dearth of real-world corroboration has been remedied in recent years as the market experienced three major declines in the span of 49 months, and this expanded sample size serves as the basis for our current study evaluating defensive ETFs in down markets.

S&P 500 Earnings Waterfall 4Q23

Analysts often address sales and net income but rarely speak to the middle lines of the income statement. Our methodology works through each major line item—from sales to net profit—comparing the most recent quarter to the same quarter of a year earlier.

Research Preview: Lost In Translation?

We are curious if factor ETFs have provided downside protection in recent years’ selloffs or whether their defensive nature, shown by academic studies, is lost in the translation to live-money portfolios.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue