Articles by Scott Opsal Chief Investment Officer

The Stock Market’s Clark Kent

.jpg?fit=fillmax&w=222&bg=FFFFFF)

Mild-mannered and humdrum on the surface but a superhero underneath—that’s Clark Kent and, in recent months, the Low Volatility factor. Low Vol stocks are unexciting by definition, and the factor’s current holdings focus on utilities, REITs, and insurance companies.

Portfolio Positioning: Deciding Not To Decide

One portfolio strategy that attracts our interest is a barbell between Growth or Quality on the bullish side, paired with a Low or Minimum Volatility sleeve for the bearish side. This approach deals with today’s uncertainties by essentially “deciding not to decide.”

Leuthold Quick Takes: Getting Sentimental

This issue of Leuthold Quick Takes reviews the conflicted nature of investor sentiment as seen by Doug Ramsey (Chief Investment Officer) and Jim Paulsen (Chief Investment Strategist).

Factor Tilts at Mid-Year

_Page_1.jpg?fit=fillmax&w=222&bg=FFFFFF)

Factors provide investors with the ability to shift their portfolio’s characteristics to fit a particular economic and market outlook. Value might look appealing under one set of conditions while Quality might be more desirable in another. We developed a research platform that analyzes various drivers of factor returns, summarized in Exhibit 1.

Lessons From The Old Masters: John Neff

A recent trip to the Netherlands included visits to The Rijksmuseum and The Mauritshuis to view paintings including The Night Watch, widely acclaimed as Rembrandt’s greatest work, and Vermeer’s equally celebrated Girl with a Pearl Earring.

Lessons From The Old Masters: John Neff

We believe the results of every investment operation depend, more than anything else, on the quality of the investment philosophy and process that drives the portfolio.

Can Smart Analysts Generate Smart Beta?

One of the virtues of quantitative investing is that it relies on measurable data points that fit smoothly into mathematical models.

Can Smart Analysts Generate Smart Beta?

We assess the effectiveness of using Wall Street analyst opinions as factors in a quantitative stock selection model. Watch for the full report coming next week.

Estimating the Downside - June 2019

The S&P 500 tumbled 6.6% in May, erasing the previous two months’ gains.

First Quarter Earnings Waterfall

What a difference a year makes! In early 2018 we were celebrating 20% earnings growth, driven by a strong economy and the massive corporate tax cut. Sales were rising at a double-digit rate and the tax burden was shrinking dramatically, setting up one of the best earnings years in history.

Signs Of Spring For Financials

Signs of spring are popping up everywhere in the Financials sector. S&P Financials was easily the top- performing sector in April and several sub-industries have been bubbling higher in our Group Selection discipline.

Factor Frontiers And Investing To The Max

Quantitative investing has taken the industry by storm over the last decade, and smart beta ETFs are pulling in billions of dollars as investors and advisors gravitate to this portfolio management technique.

So Long Tax Cuts… We Hardly Knew Ye

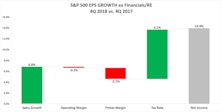

Our earnings waterfall analysis for the fourth quarter tells a story consistent with the entirety of 2018: earnings growth was fantastic, boosted by the twin drivers of strong sales growth and a lower corporate tax rate. Chart 1 spotlights the quarter’s tally, which produced a healthy sales growth number despite some economic weakening.

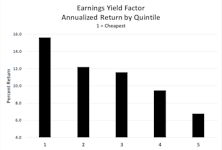

Price To Book: The King Is Dead

Since the earliest days of security analysis—when the main question was which railroad stock to buy—Price to Book has been a cornerstone of the valuation process.

Momentum Buyers: Beware

Momentum is a smart beta factor that gives investors excellent upside participation in rising markets. Most other smart beta factors are defensive plays, so Momentum is the place to be in strong upward moves. Momentum filled that role admirably in recent years, rising 56% from 2016 to the September top, compared to an average of +26% for the other major factors.

“Four Corners” Cloud Plays

The Social/Mobile/Cloud theme (SMC) has dominated the stock market in recent years, eventually reaching a frenzied peak in the summer of 2018.

John Bogle: Investment Philosopher

The passing of investment legend John Bogle has brought forth many well-deserved tributes to his professional accomplishments. He was a tireless champion of passive investing and the founder of The Vanguard Group which, as more than a few investors don’t realize, also manages almost $1 trillion in active funds.

Leuthold Quick Takes: Cyclical Bear Or Recovery Refresh?

The fourth quarter selloff and subsequent rebound, as seen by Doug Ramsey (Chief Investment Officer) and Jim Paulsen (Chief Investment Strategist).

Leuthold Quick Takes: Cyclical Bear Or Recovery Refresh?

The fourth quarter selloff and subsequent rebound, as seen by Doug Ramsey (Chief Investment Officer) and Jim Paulsen (Chief Investment Strategist).

Incongruities In High Quality

Quality is one of the most popular and successful of the equity market’s quant factors. It is intuitively appealing and serves as a useful defensive strategy in falling markets. Low Volatility and Dividend Growth are also defensive factors, while Momentum and High Beta are viewed as aggressive or bullish factors. These offsetting behaviors would seem to make for excellent diversification opportunities in equity portfolios, and for the most part, that is true.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue